Alpha Discovery · Risk Management

#24 How to Set Stop-Loss Rules for Early Breakout Entries

04/16/2026 · 5 min read

Live capture of Breakout Radar with stop levels in Inveflo.

📍 Home › ANALYSIS_1 › Early Breakout Scanner

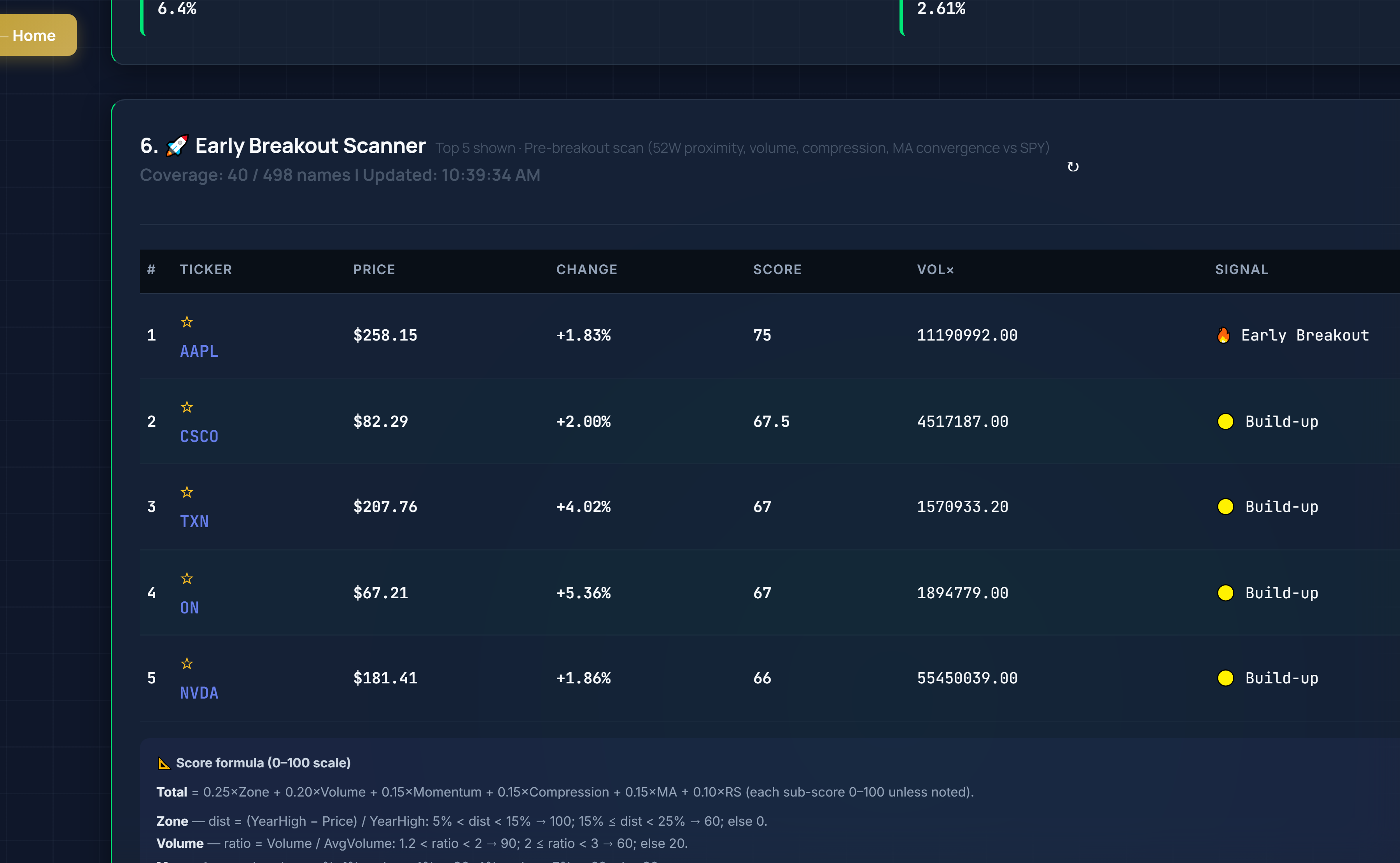

0) Where to Find This Widget

In Early Breakout Scanner or individual stock deep dive, stop levels are calculated and displayed automatically based on mechanical rules.

Live capture of Dashboard in Inveflo.

1) TL;DR

Stop rules: (1) Below breakout level = most effective; (2) At 5-day low = tighter control; (3) Below 20-day MA = room-to-run. Pick one. Always size to keep risk constant (3% per trade).

2) Hook (Pain-Driven)

I've been stopped out of winning breakouts because my stop was too tight. I've also held losers too long because I had no stop rule. Mechanical stops eliminate both mistakes.

3) Problem

Tight stops = whipsawed out of winners. Wide stops = uncontrolled losses. Without a rule, you guess. You need a mechanical placement rule that keeps risk constant (3% loss = same loss size on all trades).

4) Solution (Widget Introduction)

Use mechanical stop rules: Below breakout level (tightest), at 5-day low (moderate), or below 20-day MA (widest/maximum room-to-run). Size position so 3% loss equals consistent dollar risk across all trades.

5) Logic Breakdown (Formula + Thresholds)

Example: $100k account, 3% risk = $3k loss max. Stop 5% below entry = 600 share size.

- Rule 1: Stop Below Breakout Level Tightest stop. Breakout fails = stop out. Best for tight control.

- Rule 2: Stop at 5-Day Low Moderate stop. Allows 1-2 bar pullback. Balances room-to-run vs control.

- Rule 3: Stop Below 20-Day MA Widest stop. Maximum room-to-run but higher dollar risk. Use only on highest-conviction setups.

- Always: Size = 3% Risk Rule Position size adjusted so max loss is 3% of account. Same loss on every trade.

6) Practical Use (IF X → THEN Y)

- If CSS ≥ 80 + high conviction, then use Rule 3 (20-day MA stop). Maximum room-to-run justified.

- If CSS 60-75 + moderate conviction, then use Rule 2 (5-day low stop). Balance.

- If CSS < 60 or weak setup, then use Rule 1 (below breakout level). Tight control needed.

- If account $100k, 3% risk = $3k max loss per trade. Calculate share size = $3k ÷ distance to stop.

7) Common Mistakes

- Stop too tight (1-2%). Whipsawed on normal pullback. Result: stopped out of winners.

- Stop too wide (10%+). Uncontrolled loss if breakout fails. Result: oversize losses.

- Emotional stops. Moving stops after bad news, revenge trading. Result: destroyed discipline.

- Not sizing by 3% risk rule. Taking 5% loss on one trade, 1% on another. Result: inconsistent risk exposure.

Frequently Asked Questions

Should I move my stop up if the breakout is working?

Yes. Once stock closes 3%+ above entry, move stop to below entry to lock in breakeven. If stock reaches +8%, move stop to below 5-day low (lock in 3%+ gain). This is trailing stop discipline, not emotional. Rule: don't raise stop on decline; only raise on new highs/closes above support.

What if the 20-day MA is very far away (10%+ below entry)?

Don't use it. Cap stops at 5-7% below entry maximum, even on highest-conviction setups. 10%+ stops create uncontrolled risk. Instead, use 5-day low (Rule 2) or move below 50-day MA. Always ask: does this stop make sense for max 3% account risk? If not, don't use that rule.

How do I calculate position size using the 3% risk rule?

Formula: Position Size = (Account × 0.03) ÷ (Entry Price - Stop Price). Example: $100k account, entry $150, stop $140 = ($100k × 0.03) ÷ $10 = 300 shares. Loss if stopped = $3k (exactly 3% of account). Adjust shares to match this formula every time.

Can I break the 3% risk rule on high-conviction trades?

No. Rule exists to prevent overtrading and catastrophic losses on one bad trade. High conviction (CSS ≥85) = use Rule 3 (20-day MA), not bigger size. More conviction = better stop placement, not bigger risk. Consistent 3% risk + better stop selection = better results than larger 5-7% risk bets.

Related Posts

- #15 Early Breakout Scanner: Spotting Breakouts at Inception Breakout Detection

- #10 Risk Management for Top Picks Portfolio: Diversification and Position Sizing Risk Management

- #8 Breakout Radar: Short-Swing Template and Trade Exits Breakout Radar

CTA: Open Scanner and Find Opportunities

Scan the full S&P 500, compare quality and signal scores, and build your watch list before market open.